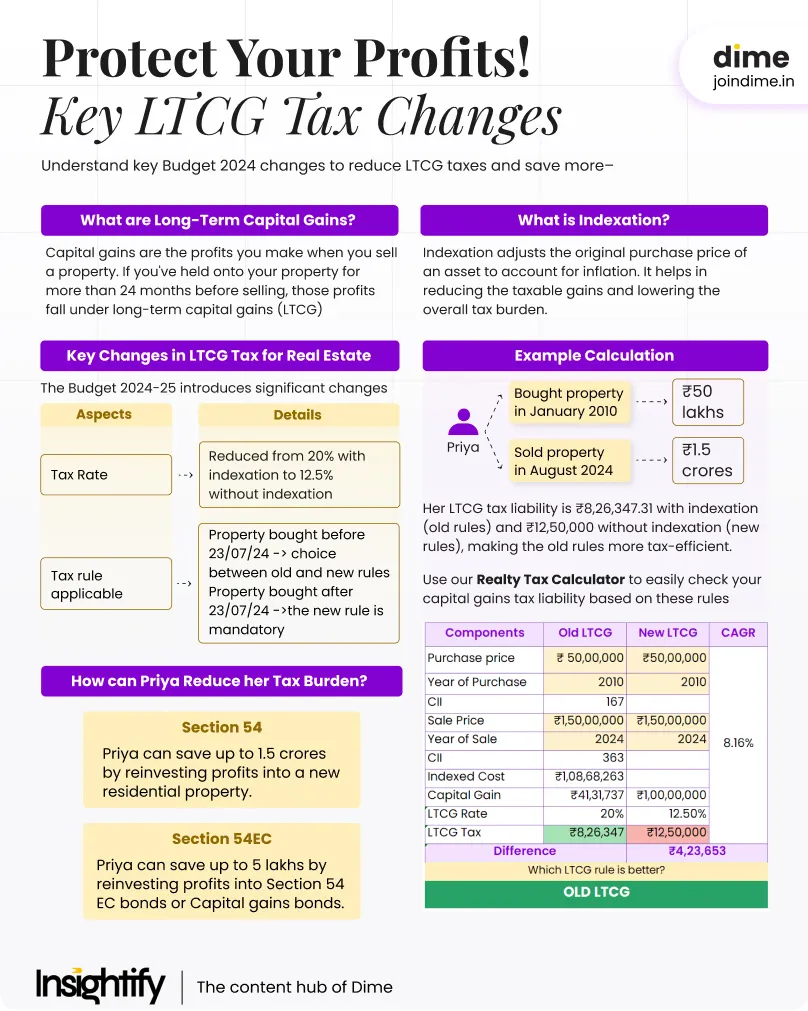

What are Long-Term Capital Gains?

Long-Term Capital Gains (LTCG) refer to profits made from selling a property held for more than 2 years. These gains are subject to special tax rates and benefits, including indexation.

Key change in LTCG taxation: Union budget 2024

But you might have an option to choose!

What is indexation, and why is it important?

Indexation is the process of adjusting the purchase price of an asset to account for inflation, ensuring that the real value of the asset is maintained over time.

By applying indexation, the taxable gains on an asset are reduced, which can significantly lower the tax liability for long-term holdings.

Understanding indexation is crucial for accurate tax planning and calculating the tax owed on long-term gains.

Calculating LTCG on real estate sale

Let’s consider a practical example to illustrate the LTCG calculation based on the new rules!

~add{5,blog_highlight-block}

Example

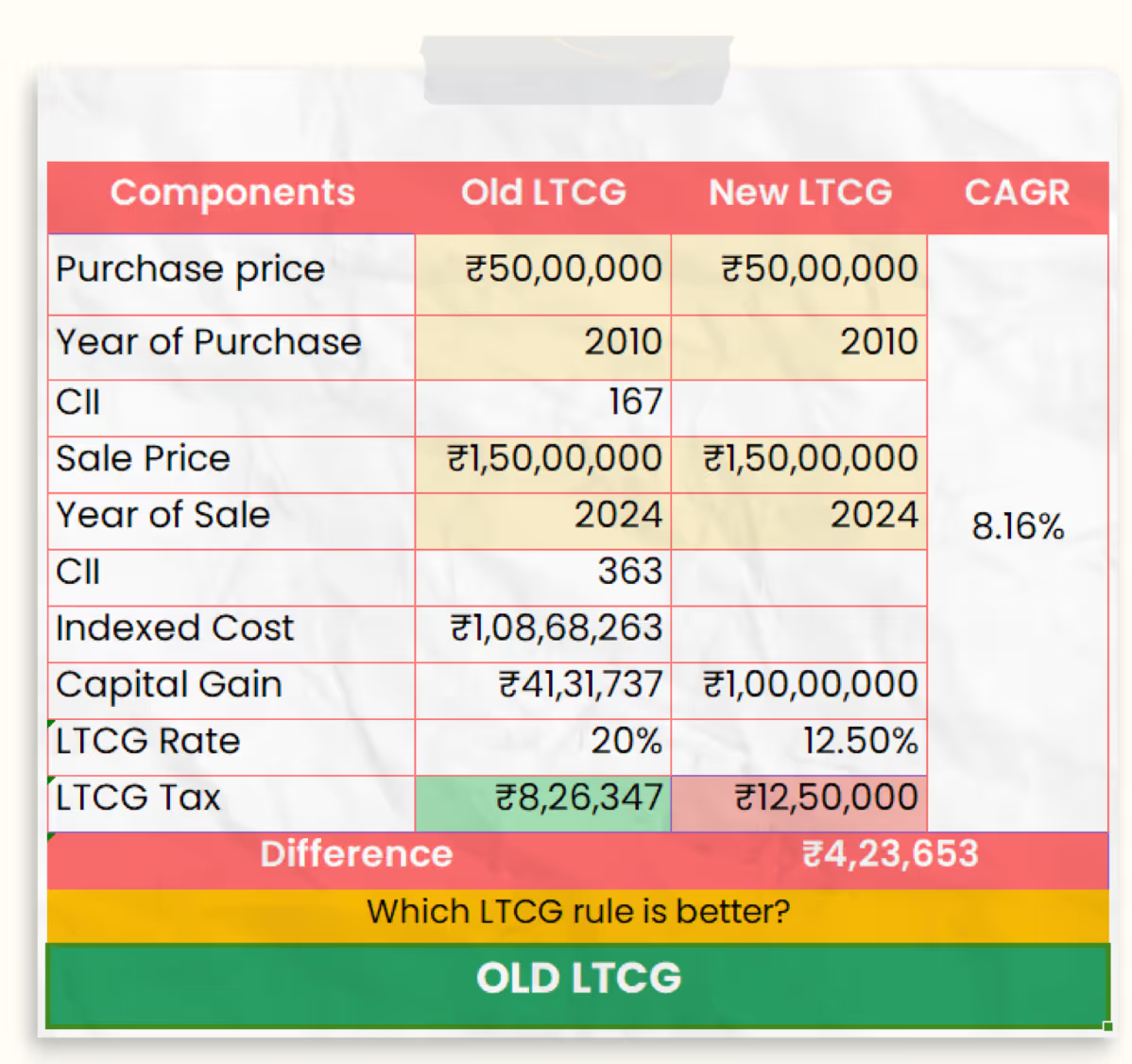

Priya, a 45-year-old professional, bought a property in January 2010 for ₹50 lakhs and sold it in August 2024 for ₹1.5 crores. Since Priya held the property for more than 24 months, it qualifies as a long-term capital asset, and the gains from the sale are subject to LTCG tax.

With the help of our Realty Tax Calculator, you can easily check your own capital gains tax liability.

Comparing old and new tax rules

- Old rules (20% with indexation): Her tax liability would be ₹8,26,347.31.

- New rules (12.5% without indexation): Her tax liability would be ₹12,50,000.

In this case, the old LTCG rules result in a slightly lower tax liability for Priya, making them the better choice.

~add{3,blog_highlight-block}

Break Even Point

Break Even point is a point where the LTCG liability is same under both the regimes.

For example, if Priya would have sold her property for ₹20,702,035, the tax under both the rules would have been same.

What is Section 54 and how can it help Priya save taxes?

Section 54 of the Income Tax Act provides tax exemption on long-term capital gains from the sale of a residential property if the gains are reinvested in another residential property within a specified period.

This benefit helps taxpayers reduce their tax liability when upgrading or purchasing a new home.

Eligibility and reinvestment requirements

By reinvesting the entire ₹50 lakh profit from the sale into a new residential property, Priya would have no LTCG tax liability. Note that if only a portion of the profit is reinvested, tax would be due on the remaining amount.

What is Section 54EC and how can it help Priya save taxes?

Section 54EC of the Income Tax Act allows the reinvestment of capital gains from the sale of property into specified bonds, providing an additional way to save on LTCG tax.

Eligibility and investment requirements

By investing ₹5 lakhs in these bonds, Priya can avoid paying LTCG tax on the amount invested.

Combining Section 54 and Section 54EC

Priya could diversify her tax-saving strategy by using Section 54 to invest in a new house and Section 54EC to invest in bonds, optimising her tax benefits.

Conclusion

Priya can minimise her LTCG tax burden by combining property reinvestment under Section 54 and bond investments under Section 54EC, ensuring smarter tax savings and maximising her profits.

~add{3,blog_highlight-block}

Summary

To make your life easier, we have summarised the above Read here. Hope you enjoyed it!

Be the CEO of your Finances

Get practical and actionable money insights delivered straight to your inbox.

.webp)

.webp)