.webp)

In India, owning a home is often seen as a necessity, while renting is viewed by many of our parents as an unwise expense.

But the numbers tell a different story!

In the last 10 years, houses have become 71% more expensive across India.

Renting a home in Bengaluru costs 4–5% of its value yearly, meaning you could own it in 20–25 years if rent were an EMI.

This leaves us wondering, is it better to buy a home or rent one?

Pros and Cons of buying/renting a house

.webp)

How to decide what’s right for you?

Here are a few numbers to consider before buying or renting a place.

~add{num,1}

Price to Income

~add{num,2}

Price to Rent

~add{num,3}

Expense to Monthly Income

~add{num,4}

Savings

~add{num,5}

Flexibility

Relocating in 5-7 years? Renting is definitely flexible and cost efficient (unless you rent out your own house).

However, the choice between renting and buying isn’t just a financial decision, it’s a reflection of your lifestyle, priorities, and future goals.

To make an informed choice, you need to ask yourself the right questions, such as:

Are you focused on wealth creation or flexibility?

What role does emotion play?

Can you comfortably afford it?

How stable are your plans?

What does the market say?

.webp)

~add{7,blog_highlight-block}

Example case study

Shah Rukh earns ₹25 lakh annually, and liked a property which costs ₹1 crore. He can choose between buying the property or renting it.

He wanted to know if he invested the downpayment amount in a mutual fund and chose to stay on rent how it would turn out financially against buying a home.

So he did the following calculation:

Assumptions

Income breakdown: 15 lakhs basic salary + 7 lakhs HRA + 3 lakhs others

Home loan tenure: 20 years

Property appreciation in Bengaluru: 7.1% YoY

Rental yield in Bengaluru: 5

Opportunity cost of investment*

Investment amount: ₹30,20,000

Returns: 11% p.a.

Investment value after 20 years: ₹2,43,48,181

Here’s what he understood!

Rent for the same property could increase from ₹37,500 to ₹99,233.33 over 20 years, However he can switch homes based on his income or needs.

EMIs are fixed, making buying a long-term commitment for which he requires financial stability throughout.

Buying is definitely more profitable, but only if he sells. Meanwhile, mutual funds remain liquid, giving him access to cash anytime.

Final verdict?

Do you actually dream of buying a home just to sell it for profit?

For most of us, a house isn’t just an asset, it’s a deeply sentimental investment tied to family, security, and pride, things that can’t be measured in numbers!

There’s no better or wiser option, it all depends on your choices and preferences.

But choose wisely and don’t fall for assumptions, because whether bought or rented, your home is where your life truly unfolds so consider every aspect in-depth.

~add{3,blog_highlight-block}

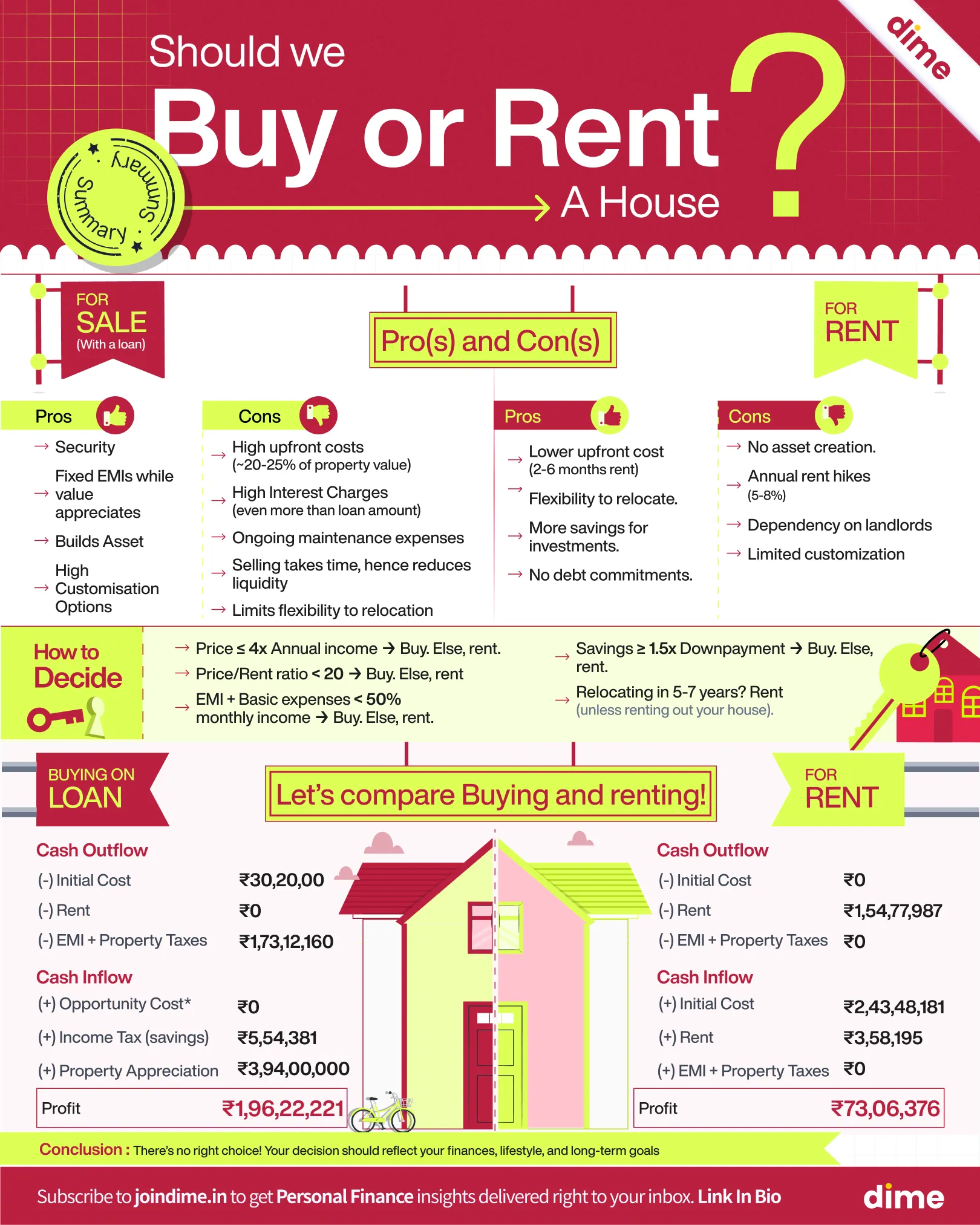

Summary

To make your life easier, we have summarised the above Read here. Hope you enjoyed it!

Be the CEO of your Finances

Get practical and actionable money insights delivered straight to your inbox.

.webp)

.webp)