Here’s a conversation tax advisors might not want you to listen to (after all they are going to make money out of it).

2024 brought significant changes to income tax rules, which will directly impact how you file your Income Tax Return (ITR) in 2025.

Here’s a detailed breakdown of the key changes and what it means for you.

~add{num,1}

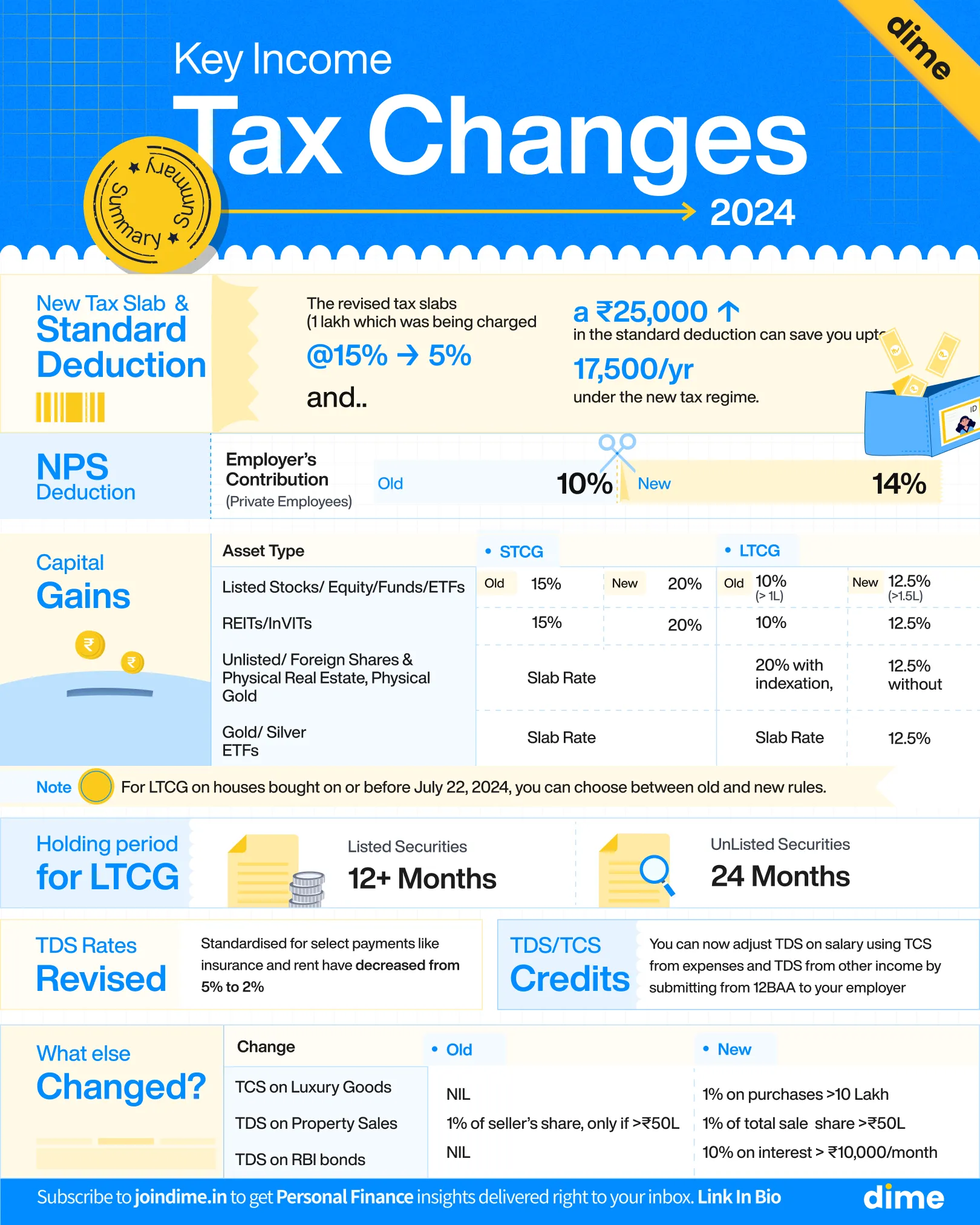

New income tax slabs

The income tax slabs under the new tax regime have changed.

Here’s how:

Basically, 1 Lakh which was being charged at 15% has been moved down to 5%.

~add{num,2}

Hike in standard deduction

The standard deduction limit under the new tax regime has increased from ₹50,000 to ₹75,000 for salaried individuals and from ₹15,000 to ₹25,000 for family pensioners.

This change reduces taxable income and benefits those opting for the new tax regime.

Note: There is no change in the standard deduction limit if an individual opts for the old tax regime.

~add{num,3}

Higher deduction for NPS contributions

Employer contributions to the National Pension System (NPS) for Private employees are now deductible up to 14% of basic salary (earlier 10%), under the new tax regime.

Note: Besides the standard deduction, this is the only deduction you can claim under the new tax regime.

~add{num,4}

New capital gains tax rules

Capital gains tax rules have been simplified to make it easier for you to calculate your income tax liability on capital gains.

Here’s how it has changed:

Note: For LTCG on houses bought on or before July 22, 2024, you have the option to choose between old and new rules. However if sold on or before July 22, 2024, the old rule is mandatory.

~add{num,5}

Simplified holding periods for capital gains

Earlier, the rules for determining long-term or short-term capital gains varied across asset types. Now, it has been simplified.

This change makes it simpler to track holding periods and plan your investments effectively.

~add{num,6}

What changed in TDS and TCS?

This year saw many changes in the rules for TDS and TCS.

Let’s have a look at them one by one:

~add{3,blog_highlight-block}

A. New TDS rates

The TDS rates have been standardised for certain payments.

Here’s how it looks now:

~add{2,blog_highlight-block}

B. Claiming TDS/TCS credit

Suppose you buy a laptop worth ₹2 lakh, and 5% TCS of ₹10,000 is collected. Now you can claim this ₹10,000 to reduce TDS on your salary by using Form 12BAA.

Additionally, the government now allows TCS credit to be claimed by someone other than the collectee. For instance, parents paying tuition fees for their children studying abroad can claim TCS credits on the payment.

These changes can help you reduce TDS deductions, improve cash flow, and get more money in hand.

Note: The TCS credit rule will take effect from January 1, 2025.

~add{2,blog_highlight-block}

C. What else changed?

Altogether, these updated tax rules aim to streamline processes and bring clarity.

Take your time to review these changes, plan your finances, and make informed decisions.

~add{3,blog_highlight-block}

Summary

To make your life easier, we have summarised the above Read here. Hope you enjoyed it!

Be the CEO of your Finances

Get practical and actionable money insights delivered straight to your inbox.

.webp)

.webp)